|

Monday, April 02 2018

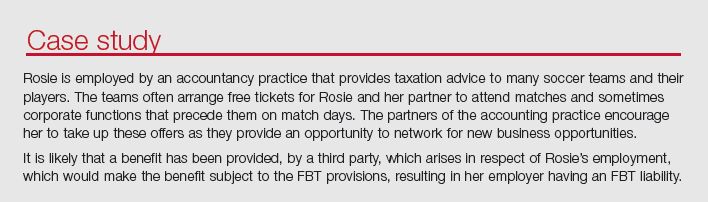

For fringe benefits tax (FBT) to apply, the conventional wisdom is that the benefits involved are provided instead of cash salary, and further that such benefits are usually paid in respect of an employment relationship. Hence the pool of accepted FBT-attracting items - laptops, cars, entertainment expenses and so on. But as mentioned, it has often been the case that employer taxpayers have made the mistake of assuming that because a benefit is provided by "someone else", they are not liable for FBT - that is, where non-cash components of remuneration are sourced from an associate, a related company or from a third-party. The arranger provisions The FBT law provides that an employer can be liable for FBT even if benefits are provided to staff by third parties or by an "associate" of your business. In other words, there could still be an FBT liability even if it is being provided indirectly. For example, arrangements to which these provisions might apply would include employees who receive goods directly from your suppliers, For a liability to arise, it is generally accepted that you must have been party to the arrangement or had been knowingly facilitating the provision of the benefit. In some cases, allowing an employee to receive a benefit in these circumstances may be sufficient to result in it being considered an arrangement for FBT purposes. Arranger provisions and meal entertainment It is not necessarily the case that you would be held liable for FBT for meal entertainment where you merely allow an employee to, for example, go out to lunch with a client where the client provides the meal, or to attend a function provided by a third party. Where you need to be careful however is where it could be inferred that an employer "entered into an arrangement" with a third party that includes providing such a benefit to your staff member, such that:

Specifically "outside" the FBT net Certain family arrangements may not necessarily trigger FBT. The ATO has ruled out a number of specific examples of benefits under family arrangements that it deems to be outside the scope of FBT law. These include:

SHARE NH BUSINESS & TAXATION NEWS Comments:

|